Opportunities in credit sectors

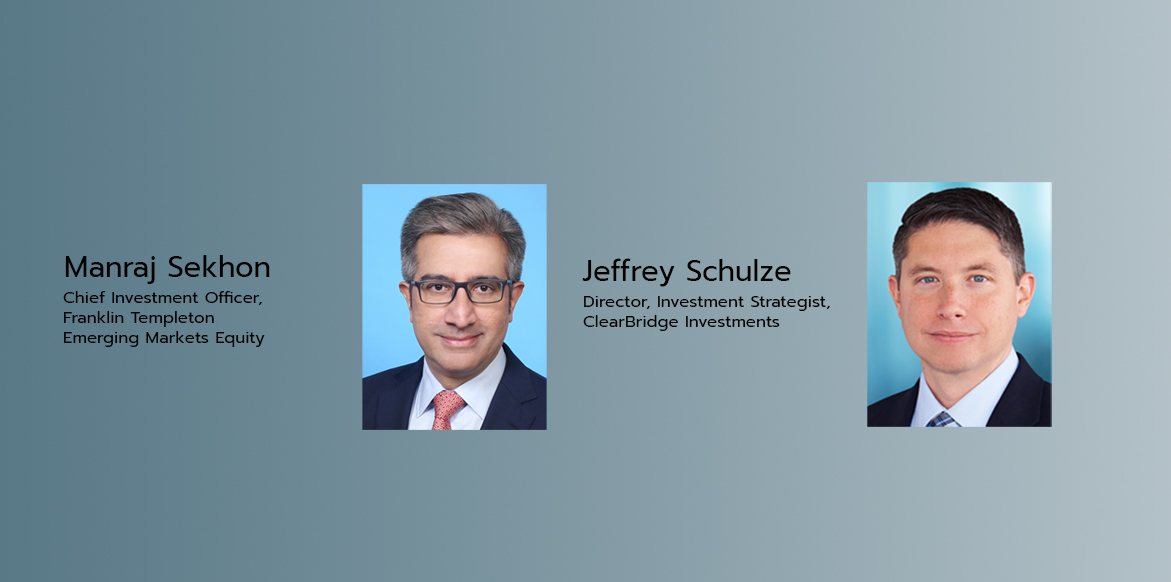

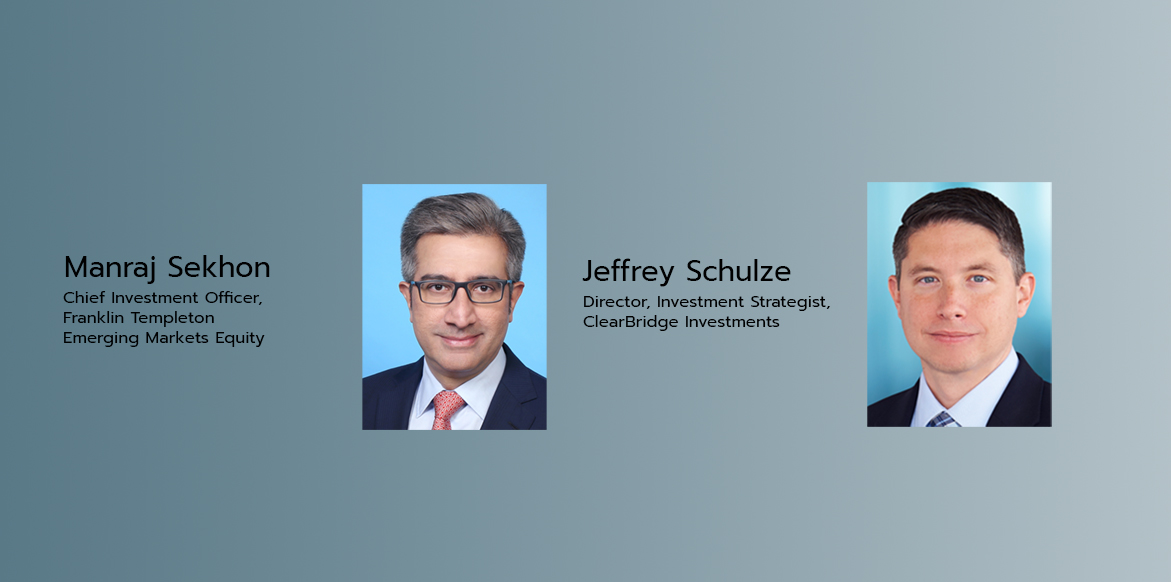

Opportunities in credit sectors Franklin Templeton and the firm’s specialist investment manager ClearBridge Investments hosted a panel session on Equities together. Investment experts from the firm including Jeffrey Schulze, Director, Investment Strategist, ClearBridge Investments and Manraj Sekhon, Chief Investment Officer, Franklin Templeton Emerging Markets Equity shared their latest observations on the upcoming risks and opportunities as we transition to a post-pandemic world and take into account a hydra of supply bottlenecks, surges in commodity prices and labor shortages that are boosting inflation, moderate growth and the Fed’s hawkish interest rate hikes.

Franklin Templeton and the firm’s specialist investment manager ClearBridge Investments hosted a panel session on Equities together. Investment experts from the firm including Jeffrey Schulze, Director, Investment Strategist, ClearBridge Investments and Manraj Sekhon, Chief Investment Officer, Franklin Templeton Emerging Markets Equity shared their latest observations on the upcoming risks and opportunities as we transition to a post-pandemic world and take into account a hydra of supply bottlenecks, surges in commodity prices and labor shortages that are boosting inflation, moderate growth and the Fed’s hawkish interest rate hikes.เมื่อเร็ว ๆ นี้แฟรงคลิน เทมเพิลตัน ได้จัดงานเสวนาด้านการลงทุนในหัวข้อการลงทุนที่โดดเด่นของโลกยุคปัจจุบันที่ส่งผลต่อการเปลี่ยนแปลงของบรรยากาศการลงทุนทั่วโลก โดยมีผู้เชี่ยวชาญด้านการลงทุนจากบริษัทต่าง ๆ อาทิ Western Asset และ Brandywine Global ให้ข้อมูลด้านการลงทุนในแง่มุมต่าง ๆ ในระดับโลก ที่นักลงทุนไทยควรจับตามองและศึกษาอย่างใกล้ชิด

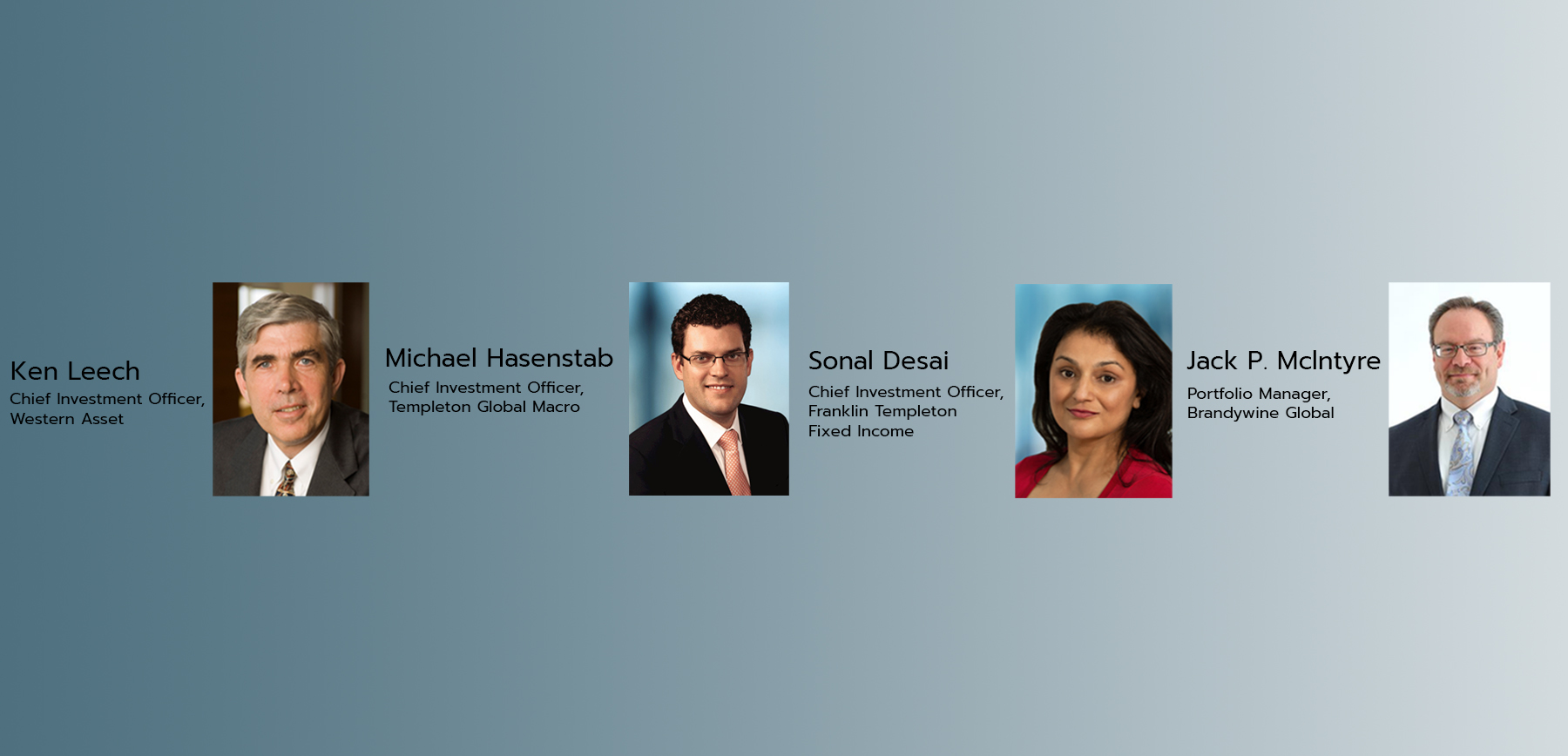

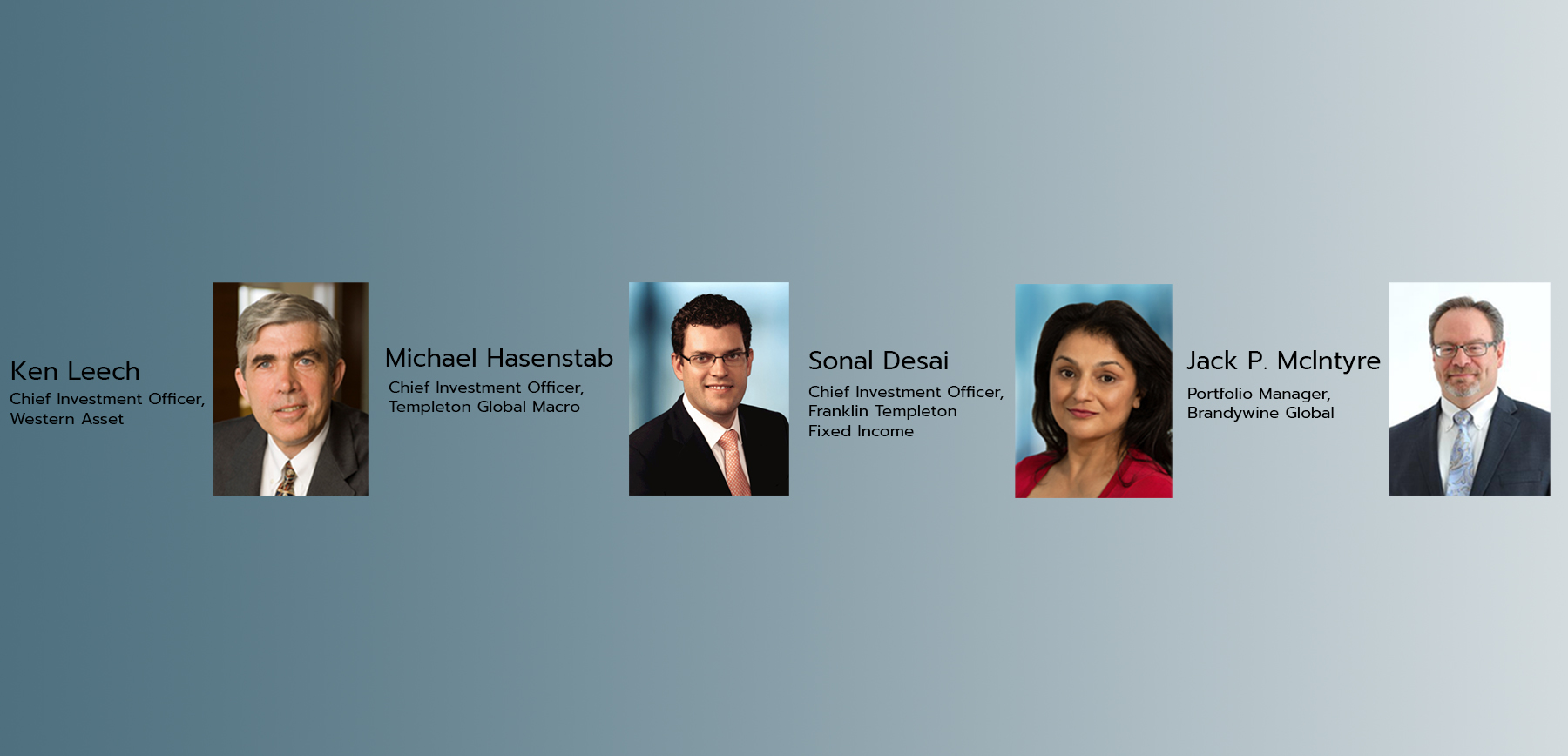

บทความพิเศษนี้ประกอบด้วยเนื้อหา 2 ส่วนด้วยกัน ได้แก่ ความเสี่ยงเงินเฟ้อและนโยบายระดับมหภาค: ที่นำมาสู่การเปลี่ยนแปลงสำคัญต่อกระบวนทัศน์การลงทุน ที่พูดถึงการเปลี่ยนแปลงระดับมหภาคและความเสี่ยงที่นักลงทุนต้องเผชิญ พร้อมชี้โอกาสการลงทุนในตลาดตราสารหนี้ โดยผู้เชี่ยวชาญด้านการลงทุนของบริษัทฯ ประกอบด้วย มร. เคน ลีช ประธานเจ้าหน้าที่บริหารด้านการลงทุนของ Western Asset มร. ไมเคิล ฮาเซนสตาบ ประธานเจ้าหน้าที่บริหารด้านการลงทุนของ Templeton Global Macro มิส โซนาล เดซาย ประธานเจ้าหน้าที่บริหารด้านการลงทุนของ Franklin Templeton Fixed Income และ มร. แจ็ค พี. แมคอินไทร์ ผู้จัดการพอร์ตโฟลิโอจาก Brandywine Global

โดยในส่วนที่สองเป็นเนื้อหาเกี่ยวกับความปกติใหม่ในอีกรูปแบบ: แนวโน้มตราสารทุนในโลกหลังการแพร่ระบาด โดย มร. เจฟฟรีย์ ชูลซ์ ผู้อำนวยการด้านกลยุทธ์การลงทุน จาก ClearBridge Investments และ มร. มาณราช ซีคอน ประธานเจ้าหน้าที่บริหารด้านการลงทุนจาก Franklin Templeton Emerging Markets Equity ที่มาร่วมแบ่งบันผลสำรวจล่าสุดทั้งในด้านความเสี่ยงและโอกาสใหม่ ๆ ตามที่เราปรับตัวไปสู่โลกหลังการแพร่ระบาด และคำนึงถึงปัญหาคอขวดของอุปทานต่าง ๆ ทั้งราคาสินค้าโภคภัณฑ์ที่พุ่งสูงขึ้น และการขาดแคลนแรงงานที่ส่งผลต่อเงินเฟ้อ การเติบโตระดับปานกลาง และการปรับขึ้นอัตราดอกเบี้ยของธนาคารกลางสหรัฐฯ

ความเสี่ยงด้านเงินเฟ้อและนโยบายมหภาค: นำไปสู่การเปลี่ยนแปลงกระบวนทัศน์ที่มีความสำคัญ

โอกาสต่าง ๆ ในภาคของสินเชื่อ

โอกาสต่าง ๆ ในภาคของสินเชื่อ

โดย มร. เคน ลีช ประธานเจ้าหน้าที่บริหารด้านการลงทุนของ Western Asset

- ในขณะที่เรื่องของสินเชื่อในปีก่อนจะเน้นไปที่ระดับของการลงทุน แต่ปีนี้ได้เปลี่ยนไปยังสิ่งที่เราอาจเรียกว่า Plain Vanilla High Yield ที่ให้ผลตอบแทนสูง เรากำลังนำการลงทุนส่วนเกินบางส่วนไปใส่กับการลงทุนในภาคส่วนที่กลับมาเปิดใหม่

- ระดับการลงทุนในพันธบัตรของธุรกิจพลังงานยังคงเป็นความสนใจหลักในพอร์ตโฟลิโอของเรา เนื่องจากเราคาดว่าจะมีการปรับอันดับความน่าเชื่อถือของบริษัทด้านพลังงาน

- เราเห็นโอกาสการลงทุนในบริษัทพลังงานที่เสมือนนางฟ้าตกสวรรค์ เนื่องจากราคาหุ้นพลังงานจะยังคงระดับเดิมอยู่อย่างเหนียวแน่นไปอีกระยะหนึ่ง และการปรับตัวด้านราคามักมีความสำคัญเสมอ

- เราใช้แนวทางที่เฉพาะเจาะจงไปที่บริษัทเพื่อมุ่งไปสู่ผลิตภัณฑ์ที่มีรูปแบบชัดเจน ซึ่งเราเชื่อว่าในอนาคตก็มียังมีข้อดีอยู่ ตามที่คาดว่าหลักทรัพย์ค้ำประเภทที่มีที่อยู่อาศัยค้ำประกันจะได้รับประโยชน์จากมูลค่าของหลักประกันที่แข็งแกร่งในสหรัฐอเมริกา

ความเสี่ยงและโอกาสการลงทุนในตลาดเกิดใหม่

โดย มร. ไมเคิล ฮาเซนสตาบ ประธานเจ้าหน้าที่บริหารด้านการลงทุนของ Templeton Global Macro

- อัตราการได้รับวัคซีนที่เพิ่มขึ้นในตลาดเกิดใหม่เป็นตัวกำหนดทิศทางที่สำคัญให้แก่การจัดการและการใช้ชีวิตร่วมกับ Covid-19 โดยเฉพาะอย่างยิ่งในภูมิภาคเอเชียที่เรามองว่ากำลังเริ่มต้นการฟื้นตัวและมีการพัฒนาใหม่ ๆ เกิดขึ้นเพื่อสนับสนุนการกลับมาเติบโตของเศรษฐกิจภายในประเทศหลังซบเซาในช่วงเก้าเดือนที่ผ่านมา

- เราคาดว่าตลาดการลงทุนในภูมิภาคเอเชียจะกลับมามีชีวิตชีวาอีกครั้งในปี 2564 ด้วยการเติบโตภายในประเทศและการค้าขายที่กลับมาเปิดใหม่ เนื่องจากภูมิภาคนี้ได้รับการคาดว่าจะมีการเติบโตอย่างแข็งแกร่งที่สุดในโลก และมีมูลค่าเกินดุลบัญชีเดินสะพัดขนาดใหญ่

ภาวะเงินเฟ้อในขณะที่เศรษฐกิจชะลอตัว (Stagflation)

โดย มิส โซนาล เดซาย ประธานเจ้าหน้าที่บริหารด้านการลงทุนของ Franklin Templeton Fixed Income

- หากกล่าวถึงภาวะเงินเฟ้อในช่วงเศรษฐกิจชะลอตัว จะเห็นว่าอัตราเงินเฟ้อนั้นลดลงต่อเนื่องมาหลายทศวรรษแล้ว และในช่วงสิบห้าปีที่ผ่านมา ความกังวลที่เด่นชัดที่สุดคือภาวะเงินฝืดที่เกิดขึ้นจากเหตุผลหลายประการในระยะยาว ซึ่งธนาคารกลางสหรัฐ (FED) ได้รับคำชมจากมาตรการปรับลดอัตราเงินเฟ้อ แต่ความเข้มข้นในการลงทุนวันนี้นั้นน่าตกใจเพราะตลาดเวลานี้ไม่เหมือนตลาดเดิม ๆ ที่เคยรู้จักกัน

- นอกจากนี้ยังน่ากังวลว่าหากอัตราเงินเฟ้อยังคงสูงและกินระยะเวลายาวนานกว่าที่เฟดคาดการณ์ไว้ เราคาดว่าอัตราเงินเฟ้อแบบดั้งเดิมในเอเชียจะมาจากปัญหาต่าง ๆ เช่น ราคาสินค้าโภคภัณฑ์และปัญหาคอขวดในห่วงโซ่อุปทาน ซึ่งเริ่มส่งผลกระทบในทางลบให้เห็นแล้ว

การลงทุนในภาคอสังหาริมทรัพย์ของจีน

โดย มร. แจ็ค พี. แมคอินไทร์ ผู้จัดการพอร์ตโฟลิโอจาก Brandywine Global

- เราคิดว่าปีหน้าจะเป็นปีที่สำคัญอย่างยิ่งภายใต้บทบาทการเป็นผู้นำของประธานาธิบดีสีจิ้นผิง เนื่องจากแรงกดดันในด้านการพัฒนาอสังหาริมทรัพย์ที่ลดลงและความไว้วางใจจากภาวะเศรษฐกิจที่ถดถอยอย่างรุนแรง

- ภาพรวมตลาดอสังหาริมทรัพย์ในประเทศจีนไม่แนะนำให้ปรับลดระดับหนี้สินจากการเทขายทรัพย์สินอย่างรวดเร็ว เช่นเดียวกันกับผลกระทบทางการเงินที่เกิดจากการแพร่ระบาดต่อเศรษฐกิจโลกที่ขยายไปในวงกว้าง

- ประเทศจีนต้องกลับไปเป็นผู้ขับเคลื่อนการเติบโตที่ใหญ่กว่าเดิม ไม่ว่าจะเป็นการขับเคลื่อนการเติบโตในแบบออร์แกนิกหรือยังต้องการมาตรการกระตุ้นเพิ่มเติมทางการเงินและการคลังที่ยังคงเป็นคำถามสำคัญ

- เราหวังว่าประเทศจีนจะเริ่มแสดงนโยบายกระตุ้นการเติบโตเชิงบวกมากขึ้น อาทิ เครดิตที่ดีขึ้นและแรงกระตุ้นทางการคลัง ซึ่งจะส่งผ่านไปสู่เศรษฐกิจโลกในวงกว้าง

- พันธบัตรในตลาดที่พัฒนาแล้วยังมีน้ำหนักการลงทุนค่อนข้างต่ำ แม้การคาดการณ์ความเสี่ยงของอัตราเงินเฟ้อจะยังคงมีอยู่หรือจำเป็นต้องได้รับเป็นอัตราผลตอบแทนที่สูงขึ้น แต่ภายนอกก็มีปัจจัยของอัตราเงินเฟ้อที่ลดลงต่อเนื่องเป็นตัวบังคับ ด้วยเหตุนี้ เราจึงไม่คาดหวังว่าตลาดตราสารหนี้ที่พัฒนาแล้วจะมีภาวะตลาดหมีขนาดใหญ่

ความปกติใหม่ในอีกรูปแบบ: แนวโน้มตราสารทุนในโลกหลังการแพร่ระบาด

แฟรงคลิน เทมเปิลตัน และผู้จัดการ รวมถึงผู้เชี่ยวชาญการลงทุนของบริษัท ClearBridge Investments ได้ร่วมเป็นเจ้าภาพจัดประชุมเพื่อหารือเกี่ยวกับทิศทางตลาดหุ้นร่วมกัน โดยมีผู้เชี่ยวชาญด้านการลงทุนจากบริษัทเข้าร่วม ได้แก่ มร. เจฟฟรีย์ ชูลซ์ ผู้อำนวยการด้านกลยุทธ์การลงทุน จาก ClearBridge Investments และ มร. มาณราช ซีคอน ประธานเจ้าหน้าที่บริหารด้านการลงทุนจาก Franklin Templeton Emerging Markets Equity มาแบ่งปันข้อมูลการลงทุนล่าสุดเกี่ยวกับความเสี่ยงและโอกาสที่กำลังจะเกิดขึ้นในโลกหลังการแพร่ระบาด โดยพิจารณาถึงปัญหาคอขวดของอุปทาน ราคาสินค้าโภคภัณฑ์ที่พุ่งสูงขึ้น และการขาดแคลนแรงงานซึ่งส่งผลต่ออัตราเงินเฟ้อ การเติบโตระดับปานกลาง และการปรับขึ้นอัตราดอกเบี้ยอย่างรวดเร็วของธนาคารกลางสหรัฐฯ

คาดการณ์อัตราดอกเบี้ยและเงินเฟ้อพุ่งสูงขึ้น

คาดการณ์อัตราดอกเบี้ยและเงินเฟ้อพุ่งสูงขึ้น

โดย มร. เจฟฟรีย์ ชูลซ์ ผู้อำนวยการด้านกลยุทธ์การลงทุน จาก ClearBridge Investments

- อัตราความเร็วที่เพิ่มขึ้นของดอกเบี้ยที่ปลายทางของเส้นโค้งจะเป็นตัวกำหนดทิศทางตลาดว่าจะดำเนินไปอย่างไร เราคาดว่าเส้นโค้งของดอกเบี้ยจะขึ้น และตลาดตราสารทุนจะเป็นกุญแจสำคัญที่สร้างผลกำไรให้เติบโตอย่างแข็งแกร่งจากกิจกรรมทางเศรษฐกิจที่ดีขึ้นที่คาดการณ์ไว้ในอีกห้าไตรมาสข้างหน้านี้

- นอกจากนี้เรายังมองว่า อัตราผลตอบแทนพันธบัตรรัฐบาลสหรัฐอายุ 10 ปีจะเพิ่มขึ้นในปีหน้า แม้ว่าอัตราดอกเบี้ยจะเพิ่มขึ้นเมื่อธนาคารกลางสหรัฐยกเลิกโครงการซื้อพันธบัตร แต่จะมีการออกตั๋วเงินคลังเพิ่มขึ้นอีกมากเนื่องจากกระทรวงการคลังสร้างจุดยืนใหม่ร่วมกับธนาคารกลางสหรัฐฯ

- ขณะที่โลกกำลังก้าวสู่ปี 2565 สหรัฐฯ เองก็กำลังอยู่ในภาวะเศรษฐกิจที่มีแรงกดดันสูง โดยมีธนาคารกลางสหรัฐฯ เป็นผู้อยู่เบื้องหลังชัดเจน นอกจากนี้ยังมีปัจจัยทางด้านกิจกรรมทางเศรษฐกิจและการสร้างงานที่แข็งแกร่ง

แนวโน้มการลงทุนในตลาดจีน

โดย มร. มาณราช ซีคอน ประธานเจ้าหน้าที่บริหารด้านการลงทุนจาก Franklin Templeton Emerging Markets Equity กล่าวว่า

- จีนอยู่บนเส้นทางที่กำลังจะกลายเป็นเขตเศรษฐกิจที่ใหญ่ที่สุดในโลกในอีก 10 ถึง 15 ปีข้างหน้านี้ และชัดเจนว่าทางการจีนยังคงให้ความสำคัญกับการเติบโตและจะไม่ทอดทิ้งภาคเอกชน

- ด้านกฎระเบียบ ผลกระทบต่อการประเมินมูลค่าของบริษัทที่เกี่ยวข้องกับอินเทอร์เน็ตขนาดใหญ่จำนวนมากนั้นมีราคาอยู่แล้ว ผู้มีอำนาจและผู้กำหนดนโยบายกำลังใช้ความระมัดระวังเพื่อให้แน่ใจว่าช่องว่างระหว่างผู้ที่ได้รับประโยชน์จากการเติบโตดังกล่าวจะไม่กว้างไปกว่าเดิม เช่นเดียวกับเศรษฐกิจเกิดใหม่และผู้ที่ไม่ได้รับประโยชน์ในส่วนนี้

- เราเห็นเศรษฐกิจที่แข็งแกร่งมาก การสร้างความมั่งคั่ง การขยายตัวของเมือง และการเติบโตของการบริโภคอย่างรวดเร็วของกลุ่มชนชั้นกลาง หากคุณเชื่อมั่นกับประเทศจีนในภาพรวม ตอนนี้คือเวลาที่เหมาะสมในการสร้างพอร์ตสินทรัพย์ในประเทศจีนที่จะเป็นผู้ชนะของตลาดในระยะยาว

แนวโน้มการลงทุนของตลาดเกิดใหม่

โดย มร. มาณราช ซีคอน ประธานเจ้าหน้าที่บริหารด้านการลงทุนจาก Franklin Templeton Emerging Markets Equity กล่าวว่า

- มีการเติบโตอย่างก้าวกระโดดที่สำคัญในความก้าวหน้าของเศรษฐกิจใหม่ ๆ ในตลาดเกิดใหม่ ในบางกรณีเราเห็นถึงการขยายตัวของอินเทอร์เน็ต อีคอมเมิร์ซ และเทคโนโลยีดิจิทัลนั้นก้าวหน้ากว่าสิ่งที่เราเห็นในตลาดที่พัฒนาแล้ว เราคาดว่าแรงขับเคลื่อนของการเปลี่ยนผ่านไปสู่ดิจิทัลจะดำเนินต่อไป

- ขณะเดียวกัน รูปแบบใหม่ของการใช้พลังงาน ไม่ว่าจะเป็นพลังงานหมุนเวียน การผลิตไฟฟ้าสำหรับยานยนต์ หรือพลังงานแสงอาทิตย์ จะเป็นตัวขับเคลื่อนการเติบโตที่สำคัญในตลาดเกิดใหม่ โดยเฉพาะอย่างยิ่งในกลุ่มหุ้นขนาดเล็กและขนาดกลาง ครอบคลุมกลุ่มธุรกิจอย่างกว้างขวาง อาทิ ฟินเทค ระบบการชำระเงิน ค้าปลีก อีคอมเมิร์ซ พลังงานสะอาด

- ไม่กี่เดือนที่ผ่านมาบราซิลได้ประสบปัญหาอย่างหนักหน่วงจากการถูกปรับลดมูลค่าและอัตราดอกเบี้ยที่สูงขึ้น ประกอบกับความเสี่ยงทางการเมืองที่มากขึ้น แต่สถานการณ์ทางการคลังและบริษัทในประเทศนั้นแข็งแกร่งกว่าที่เราเคยเห็นในรอบก่อนหน้านี้มาก ดังนั้นเราจึงเชื่อว่ามีโอกาสที่น่าสนใจมากมายในบราซิลเมื่อพิจารณาจากการประเมินมูลค่า